Ghana has witnessed some positive actions for the country in government’s quest to achieve financial inclusion, using it to propel the kind of development people have yearned for, for decades. The first action was the announcement by the National Identification Authority (NIA) that it was ready to roll out the National Identification System. This has been on the drawing board for years and even though at some point portions were executed, it was not enough to be leveraged.

The second thing was the assurance by the government to the effect that the National Address System was being finalized. This, just like the Identification system had remained on the drawing board for far too long even though it is a known fact that the two are sine-qua-non-for the attainment of a fully digitized payment system in Ghana.

The third but perhaps the most consoling thing to occur is the release of a report by Bankable Frontier Associates, an independent consultant with funds from the Better Than Cash Alliance. The Report diagnosed the progress of digital payments and the challenges that lie ahead. The findings generally affirm that the government means business in creating an economy where everyone can pay and get paid digitally, instead of using cash.

First of all, the findings of the report show the country has made significant gains, including almost 100% of government payments to people and payments within the government is now processed digitally. It particularly predicts that if the government continues to make progress, savings could reach over GH¢250M (nearly $60 million) each year, which may result in more than GH¢1B ($230 million) by 2020, and that “for digital financial services to reach all segments of the society, Interoperability is a key and critical ingredient to evolving larger payment ecosystems”, thus according to Deputy Finance Minister, Charles Adu Boahen who spoke at the launch of the report. It cited the Government’s plan for improving the levels of financial inclusion, with good internet connectivity and expansive mobile money agent networks as an attestation to its commitment.

In 2016 for instance, the study found that mobile money merchants facilitated GH¢550M financial transactions, even though only 37 percent of the value of all payments were made digitally of the estimated GH¢561B payments processed through electronic channels annually. That meant that, on the whole, the vast majority of payments, by volume, were still made in cash – about 99.6%, and this is where the problem is, especially when it tells that “Individuals continue to purchase essential goods, including food, in the informal economy, with cash”, but more scaring is the fact that it was estimated that the annual value of GH¢5B transactions made by individuals was done through cash representing 71%, while 29% was conducted electronically.

In the view of the experts who conducted the study, improving payment Interoperability, digitizing government procurement payments and leveraging electronic fund transfer infrastructure for business-to-business payments, as well as incentivizing digital payments at the point of sale are the immediate action points which must be implemented to ensure a totally digitized electronic cashless payment system.

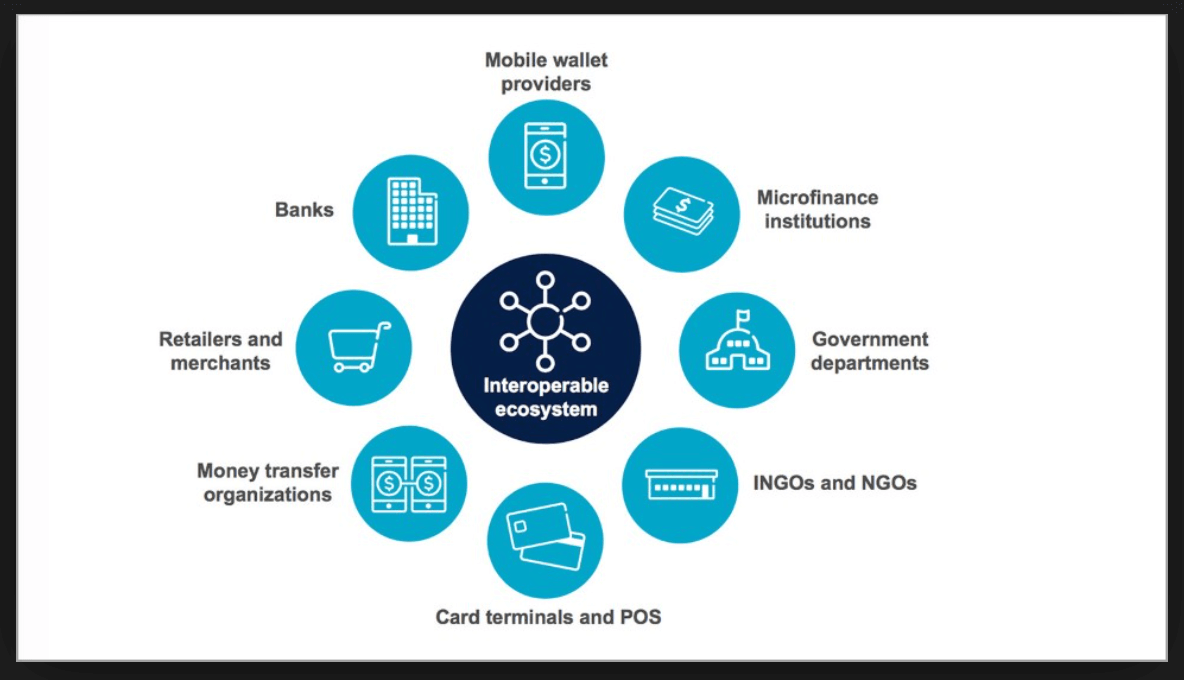

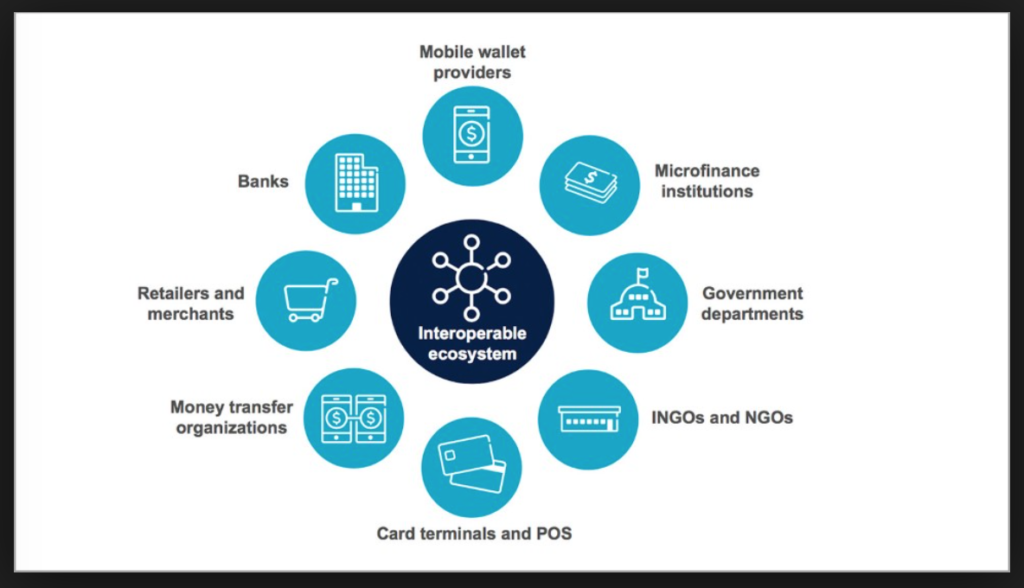

Thankfully, however, the state-of-the-art national switch built by Sibton Switch has taken adequate care of the aforementioned recommendations. This is because, as a smart grid, the fact that technology deployments must necessarily connect large numbers of smart devices and systems involving hardware and software was not lost on its operators. Simply put, Sibton has constructed a platform capable of linking multiple networks, systems, devices, applications, or components to share and readily use information securely and effectively with little or no inconvenience to the user. This is because the management of Sibton was aware of the dictates of the integrity the Ghana Retail Payment Infrastructure Systems being spearheaded by the Bank of Ghana was interested in and was equally aware that aside from the software, hardware and training challenges, ensuring an End-to-End compliance to include every stakeholder or user was non-negotiable. This is because, as a smart grid, the fact that technology deployments must necessarily connect large numbers of smart devices and systems involving hardware and software was not lost on its operators. Simply put, Sibton has constructed a platform capable of linking multiple networks, systems, devices, applications, or components to share and readily use information securely and effectively with little or no inconvenience to the user.

The Uber experience has taught us that road transportation can be made cashless. All that is required apart from the switch are perhaps mobile phones and Point Of Sale (POS) device so that whether in a Ghanaian Trotro, a taxi, a bus or public train, payment transactions are done without cash. This even reduces the risk associated with a passenger or a transport operator having to keep a large volume of cash on them. The Ports of Ghana are already paperless. The process has to be complemented with an easy electronic payment process and the ease of doing business in Ghanaian Ports will be felt by all. This enhances our image in the eyes of local and foreign investors. Even though the traditional banks have developed efficient interbank payment systems, courtesy Ghana Interbank Payment and Settlement Systems (GhIPSS), same cannot be said of rural banks, Savings & Loans entities, Microfinance, and Insurance firms, compelling patrons of their services to use cash for transactions.

Aside from having some of the world’s finest brains behind its operation and management, the Sibton Switch is a robust, guaranteed with backups, tested and proven to be flawless to ensure security, confidentiality, hacking and also prevent regular breakdowns which creates inconvenience for users largely. The other good thing is that though a privately-operated Switch, Sibton does not intend to work without close collaboration with the GhIPSS with whom they hope to share synergies.

Another grey area of concern has to do with the payment of utility bills. On a daily basis, many people are compelled to hold cash to pay bills like water, electricity, DSTV, trash or waste management, property rates, phone credits, school fees and even for transactions with the local market women. In 2004 for instance, the U.S. Department of Energy (DOE) formed the GridWise Architecture Council (GWAC) to articulate Interoperability concepts and facilitate the Interoperation of smart grid technologies. Three years later, the Energy Independence and Security Act of 2007 (EISA) gave the National Institute of Standards and Technology (NIST) the primary responsibility to coordinate development of a framework that includes protocols and model standards to achieve Interoperability of smart grid devices and systems.

In Africa too, what the Nigerian Inter-Bank Settlement Systems (NIBSS) decided to do was to provide services to the players in Mobile payments to enable them to Interoperate with banks and other financial institutions. This helps Mobile Money providers offer a wide array of services to their clients and subscribers. For example, under the Cashless Nigeria programme, the NIBSS has ensured all bills, such as school fees, electricity and water bills are paid using the e-bills pay facility which uses the payment aggregator on the Switch operated by the private sector. Kenya is an undisputed global leader when it comes to mobile money services. In 2007, the telecom operator Safaricom launched its mobile money service M-Pesa as a simple way to text small payments between users. A decade later, M-Pesa has become the world’s most successful money transfer service.

The platform enables almost 30 million people to pay for crucial services, access loans, and send money all over the world. M-Pesa is also a leading revenue generator for Kenya’s government and has spread to 10 countries, including Albania, Egypt, Romania, Lesotho, and Tanzania.

Still, in Kenya, the downside has always been the inconvenience of sending money across mobile networks. Consumers often complain that the process is tedious and expensive. Mobile operators such as Airtel have also complained that Safaricom’s dominance in the market undermines their business, and called for a leveling of the playing field, something Sibton has learned from, reason why it seeks to put in place a more efficient system to make life more convenient for Ghanaians so Ghana could be ahead of Kenya if it accelerates her processes. Even in Kenya, new Interoperability regulations are being adopted among service providers. Officials from both Kenya’s ICT ministry and the Communications Authority of Kenya have been pushing for the adoption of this regulation, allowing users to send money across networks at no additional cost. On Wednesday, May 10, 2017, at the company’s annual conference, Safaricom CEO Bob Collymore spoke in positive terms about the regulations, saying that the company “strongly” supported Interoperability and was “committed to delivering that within the next three months.” Experts today have long viewed mobile Interoperability in Kenya as inevitable. The Interoperability measures will drive financial inclusion among subscribers.

Tanzania, which set a precedent as the first African country to adopt full mobile money compatibility among its networks, has reported increased transactions among users. In Kenya, the measures are meant to also create fair competition and allow seamless interaction among the six mobile money transfer platforms: M-Pesa, Airtel Money, Orange Money, Equitel, Mobikash, and Tangaza. Beyond that, Interoperability in Ghana, just like in Kenya will allow consumers the ability to access different services in case of technical hitches. For instance, in late April, Safaricom’s network experienced a countrywide outage affecting voice calls, data, and M-Pesa services. Even though it was restored hours later, the loss of revenue and inconvenience caused an uproar.

In many countries, the big issue has been about misconceptions that Interoperability will shrink profits of service providers or let’s call them stakeholders but that is not so at all. Take the example of ATMs where a customer of any bank can use any bank’s ATM today which wasn’t the case some 10 years ago. Has that reduced the profits of banks, NO! Rather, it has reduced the cost on Banks as more people are using ATM facilities. This can even further increase if all the banks work together and divide the areas for installing ATMs used by all the customers, resulting in reduced cost with increased reach. I think in the same way if we have interoperability in mobile money, it will ultimately increase the market size and every provider would be benefitted with increased market size.

India is one of the countries where technology has facilitated a significant revolution in payment systems. It started with the mechanisation and automation of certain processes by introduction of cheque sorters and readers, MICR-based clearing, etc and moved on to the use of Information Technology for efficient funds transfer mechanisms such as Electronic Clearing System (ECS), National Electronic Fund Transfer (NEFT), Cheque Truncation System (CTS) and Real Time Gross Settlement (RTGS). The Reserve Bank of India has already initiated work towards the introduction of new generation RTGS which will be able to handle rising volumes, provide better functionalities and maintain better technological adaptability. Our journey towards leveraging technology for making our payment systems at par with the best in the world will continue with appropriate contributions from all concerned.

Electronic payment products provide speedier, cost-effective and secure payment mechanisms to customers in comparison to traditional paper-based methods. The Reserve Bank of India has been proactively involved in promoting electronic mode payments. Electronic payment products are expected to provide speedier, cheaper and hassle-free payment experience to customers in comparison to traditional paper-based payment instruments. The evolution of electronic payment products in the country have progressed through two main phases – (i) introductory phase and (ii) rationalization phase and the RTGS system has been exhibiting rapid growth, not only in terms of volume and value of transactions but also in the coverage of branches. During the year 2009-10, a total of 11,172 bank branches were added in the RTGS system, thereby increasing the number of RTGS enabled bank branches to 66,178. Contrastingly In 2004, only 4,800 branches offered RTGS in India. The rapid acceptance of RTGS by users can be measured by the daily transaction volume: today, close to 100,000 transactions a day are settled in the RTGS mode.

Back home in Ghana, mobile money transaction volume rose to GH¢35.4B in 2016, an increment of 216 percent over the previous year. This was generated by the four mobile networks; MTN, VODAFONE, TIGO, and Airtel doing same network services alone, but from every indication, an efficient Interoperability switch could easily triple these figures when it comes onstream. Sibton is ready and it has what it takes to get revenues swelled by insisting on prudence and maintaining peace of mind in doing business for all stakeholders, the very reason the Ghana Retail Payment Infrastructure System will work and work well.

Source: Elizabeth Ofosu-Danso